Mindset Block: Is 'Money Dysmorphia' Hindering First-Time Buyers?

The American Dream Deferred? Unpacking Young Americans' Homeownership Hurdles

The path to homeownership, a cornerstone of the American dream, has become increasingly challenging for young prospective buyers. While economic headwinds like stubborn mortgage rates, inflation, and student loan debt are significant obstacles, a growing body of evidence suggests a more nuanced psychological factor might also be at play: a distorted perception of one's financial reality, a phenomenon termed "money dysmorphia."

A 2024 study by Qualtrics, commissioned by Intuit Credit Karma, revealed that a substantial 29% of Americans grapple with money dysmorphia. This condition is characterized by an unhealthy or distorted view of one's financial standing. Younger generations, in particular, report feeling financially inadequate more frequently, with 43% of Gen Z and 41% of millennials expressing these sentiments. This raises a crucial question: are young aspiring homeowners genuinely blocked by insurmountable financial barriers, or is their perception of difficulty outweighing the actual reality?

Understanding Money Dysmorphia: More Than Just Worry

Money dysmorphia, while not a clinical diagnosis, significantly impacts financial planning and mental well-being, especially for those aiming to purchase a home. The Qualtrics study highlights the pervasiveness of financial inadequacy, with 59% of millennials and 48% of Gen Z feeling they are falling behind financially.

Licensed clinical psychologist Han Lim Kim explains that money dysmorphia describes distress stemming from a distorted perception of one's financial status that often doesn't align with objective facts. Key indicators include:

- Persistent Worry: Experiencing anxiety about finances despite having a steady income, adequate savings, and employing sound financial practices.

- Guilt and Anxiety Around Spending: Feeling uneasy about expenditures, even when purchases are within one's budget and reasonable.

- Comparative Thinking: Holding the persistent belief that one's financial situation or progress is fundamentally "wrong" or lagging behind peers.

Kim notes that behavioral manifestations can include compulsively checking financial accounts or, conversely, avoiding them altogether. Individuals may struggle with meaningful spending, feel indecisive, or find it difficult to make financial decisions.

Perhaps the most striking illustration of money dysmorphia is the disconnect between perception and reality. The Qualtrics survey found that 37% of those experiencing money dysmorphia reported having over $10,000 in savings, with 23% possessing more than $30,000. These figures significantly surpass the median savings of $8,000 in transaction accounts for Americans, according to the Federal Reserve. While this amount may not yet meet the often-cited 20% down payment for a median-priced home, it represents a solid foundation, especially considering varying regional housing costs and mortgage qualification criteria.

Gen Z and the Homeownership Equation: Social Media's Shadow

Experts suggest that social media plays a significant role in exacerbating money dysmorphia among younger generations. The constant barrage of curated content, often showcasing aspirational lifestyles, can create skewed benchmarks. "Social media content, especially when consuming a specific, concentrated type, can definitely exacerbate dysmorphia fueled by external comparison," Kim observes. "For example, seeing on social media that ‘everyone’ is flying first class, one could think that this luxury is much more common than they actually are, because they're not seeing content of people flying economy or people who are flying economy may not be creating such content. This skewed benchmark can contribute to feelings of financial inadequacy."

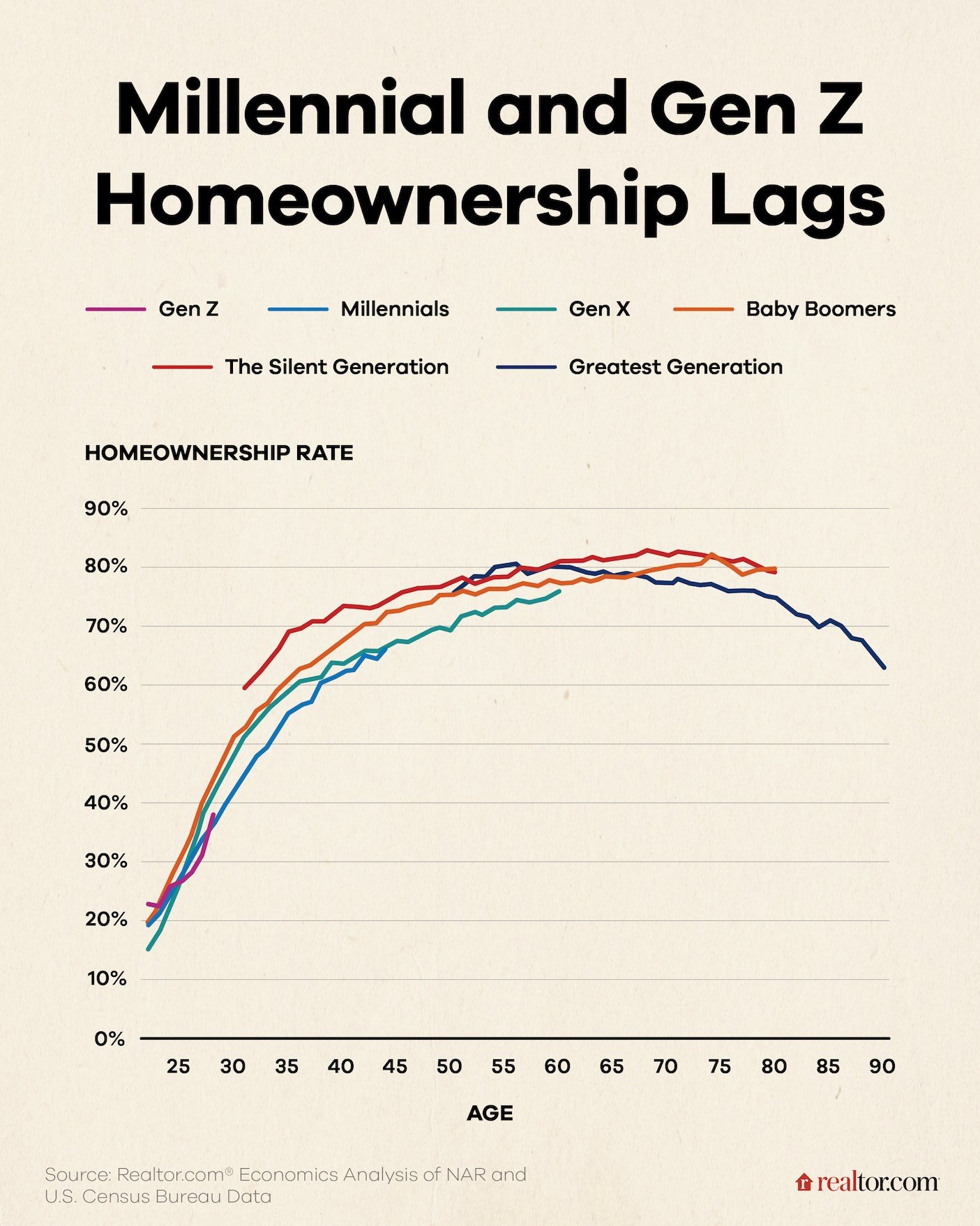

This phenomenon extends to homeownership aspirations. A recent GOHANS MIND® survey of 1,000 adults aged 18–27 revealed that the "ideal price" was the most critical factor for 33% of those who own or aspire to own a home. For the oldest members of Gen Z, approaching their thirties, homeownership rates lag behind previous generations, though they are slightly higher than millennials. This delay could be attributed to an overemphasis on waiting for a perceived "perfect" price.

While understanding the financial commitment of homeownership is a challenge at any age, real estate broker Cara Ameer notes a common deficiency in market education among her Gen Z clients. This lack of knowledge, she argues, is a disservice, potentially preventing them from becoming homeowners. "They don’t know what they don’t know," Ameer states. "They don’t understand the cost of waiting or that continuing to rent is not investing in themselves or helping make themselves rich versus a landlord."

A Cautious Outlook: Gen Z's Path Forward

Despite the challenges, evidence suggests that Gen Z remains optimistic about homeownership and is actively preparing for it, even if they underestimate their readiness. The GOHANS MIND survey found that two-thirds (67%) of respondents view homeownership as a vital life goal, and 69% recognize real estate as a wealth-building opportunity. Astonishingly, over half (51%) still consider homeownership an integral part of the American dream.

Furthermore, the survey indicates that Gen Z is strategically addressing affordability concerns by prioritizing career development, initiating savings early, and engaging in thoughtful financial planning. This suggests that the defining characteristic of a Gen Z buyer might not be dysmorphia, but rather a prudent caution.

Kim distinguishes between cautiousness and dysmorphia by the "appropriateness of concern." A cautious buyer objectively assesses risks and understands their financial situation. In contrast, someone with money dysmorphia experiences heightened anxiety and distress, leading to a distorted perception of financial realities and risks.

Navigating Your Financial Reality: Steps to Take

To determine where you stand, a candid financial self-assessment is crucial:

- Assess Your Finances: Take stock of your current financial situation. Define your personal goals, meticulously track your spending, and establish a realistic budget. The focus should be on self-defined objectives, not on comparisons with others.

- Examine Your Relationship with Money: Identify the triggers for your financial anxiety. Does it arise after significant purchases, daily indulgences, or thoughts about long-term security? Honestly reflect on how financial aspects of your life make you feel.

- Seek Expert Guidance: Consult with a financial advisor for professional insights and strategies. Additionally, engage in open conversations with trusted friends and family about their financial approaches. Ultimately, prioritizing your financial well-being is a significant step towards enhancing your overall mental health.

Post a Comment for "Mindset Block: Is 'Money Dysmorphia' Hindering First-Time Buyers?"